The Market You Think You Are Competing In Is Probably Not the Market Buying Decisions Are Made In

Most organisations could not tell you exactly when or how they decided which market they compete in. It happened incrementally. The product team named the category, the sales team defined competition by whoever they lost to, the marketing team inherited both and built a strategy around a market frame that was never consciously chosen. It was assembled, not decided.

That inherited frame shapes everything downstream: who you target, what you say, where you spend, and how you define winning. If the frame is wrong, so is the strategy built on top of it.

The Category Is Not the Market

In 1898, Elias Lewis designed the AIDA model for a world of single-channel, single-salesperson transactions. In the 1960s, McDonald’s defined its market as quick-service food. When the chain wanted to understand why milkshake sales were not growing, it surveyed milkshake buyers, tested new flavours, and improved the product based on what people said they wanted. Sales did not move.

Clayton Christensen’s team took a different approach. They spent 18 hours observing who bought milkshakes and when. What they found had nothing to do with flavour or demographics. Almost half of the day’s milkshakes were sold before 9 a.m. by solo commuters who never bought anything else. When interviewed, they all described the same job: a long, boring drive to work, a need to stay occupied, something to hold in one hand that would not spill and would keep them full until 10 a.m. Harvard Business School

The milkshake was not competing with the Burger King milkshake. It was competing with bananas, bagels, and boredom. The competitive set had nothing to do with the product category and everything to do with the situation. When McDonald’s understood this, the market was not the size of milkshake sales. It was seven times larger than the initial category estimate, it was the fast breakfast and commute market. ChristenseninstituteProductside

The product did not change. The understanding of what it was competing for did. That single reframe changed who to reach, what to say, and where to invest.

The Moment Has Already Passed by the Time Buyers Search

Most marketing strategy is built around the active buyer. The person who has typed a search query. The person filling in a contact form. The account showing intent signals in the targeting platform. This is a rational response to what is measurable. It is not a rational response to how buying actually works.

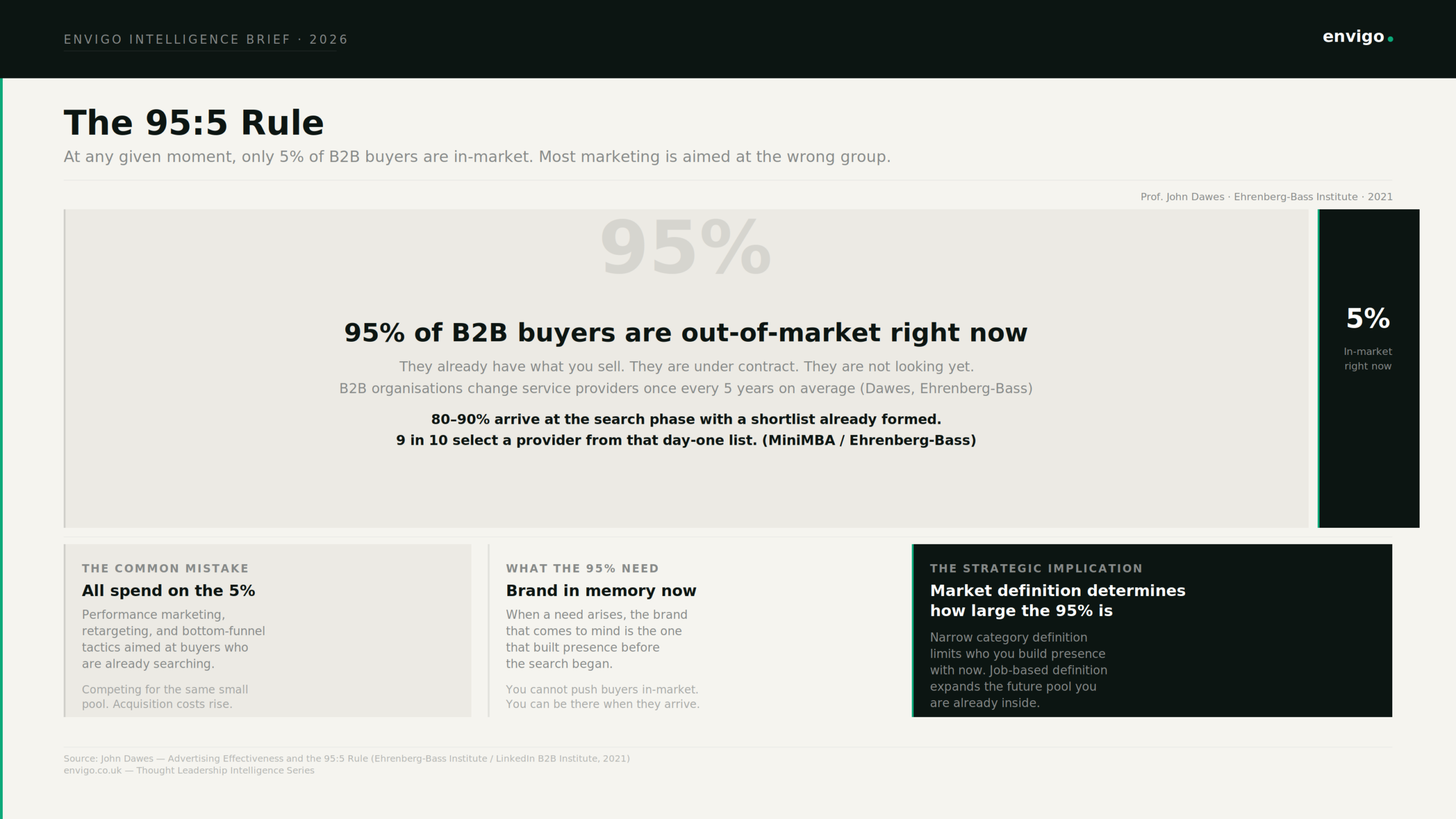

Only 5% of B2B buyers are in-market to buy at any given moment. That means 95% of the buyers any campaign reaches are not going to buy for months or years. Marketers cannot persuade a buyer to go in-market because they already have what is being sold and will not need a replacement anytime soon. Marketingscience

The research behind this is based on the average B2B purchase frequency window of five years, meaning 20% of the market is in-market in any given year, and only 5% in any given quarter. Summit Partners

This is not a reason to stop marketing to the 5%. It is a reason to understand that competing only for the 5% means competing in the most crowded, most expensive corner of the market. The moment where every competitor is also present, acquisition costs are highest, and differentiation is hardest to establish.

The more important implication is what happens before the 5% moment arrives. A recent study of B2B buyers found that 80 to 90% already had a list of vendors in mind before they began the research phase, and 9 in 10 went on to select a provider from that day-one list. The shortlist is assembled from memory, not from search results. The race is won or lost in the 95%, not the 5%. By the time a buyer searches, they are largely confirming a preference that was formed somewhere else. MiniMBA

Your Competitive Set Is Determined by What Buyers Recall, Not by Who You Listed in Your Competitor Slide

Mental availability is the probability that a buyer will notice, recognise, and think of a brand in buying situations. That is more than brand awareness. It is coming to mind at the moments that matter and being easily chosen when the brand does come to mind. RED C

The mechanism that determines this is what the Ehrenberg-Bass Institute calls category entry points: the situations, occasions, and triggers that bring buyers into the category. Category entry points capture the thoughts buyers have as they transition into making a category purchase. They are not product attributes. They are situational cues. The scenario, the feeling, the circumstance that makes a buyer think: I need something to solve this now. People the Brand

A B2B services firm is not recalled because of its service list. It is recalled because it was present, repeatedly, in the situations that matter to its buyers: the moment a campaign underperforms, the quarter a board wants to see ROI, the week a new competitor arrives and urgency spikes. Brands linked to those entry points in memory are in the consideration set before the buyer has opened a browser tab. Brands that defined their market narrowly around category competitors and built awareness accordingly are often invisible at that moment.

This is the practical consequence of market definition. A narrow category definition limits which entry points you try to own. A job-based definition expands them and with them, the population of future buyers your brand is present with while they are still in the 95%.

What Most Buyers Look Like

The final piece of this is who actually buys any given brand. Most sales volume for large brands comes from people who buy infrequently. Growth is usually achieved by reaching more category buyers overall, not by increasing loyalty among heavy buyers. Zappi

Most of a brand’s users are light users. Only around 13% of any brand’s buyers are solus buyers, meaning 87% of buyers are multi-brand buyers who hold the brand in a repertoire alongside competitors. They did not choose exclusively. They chose often enough, in certain situations, for reasons that were partly familiarity, partly occasion, partly what came to mind at the right moment. Ignition Blog

This matters for market definition because it changes who a growth strategy is designed for. If 87% of your buyers also buy competitors, the question is not how to build deeper loyalty among a committed core. It is how to be the brand that comes to mind across the situations in which the category need arises for a much larger population of light and non-buyers who will eventually make a choice.

Three Questions Worth Asking Before the Next Strategy Session

- What job are buyers hiring this category to do, and are there situations where that job arises that we are not present in? The milkshake research found a market seven times larger than the category suggested. Most organisations have not seriously asked this question.

- Which category entry points does our brand need to be associated with in buyer memory, and how do we currently perform against those entry points? Measurement matters here. Top-of-mind awareness is not the same as mental availability. The approach measures a brand’s share of customer entry point-brand linkages across the category, not just whether buyers can recall the name unprompted, but whether they recall it in the situations that trigger a purchase.

- What proportion of our marketing investment is reaching the 95% of future buyers who are not in-market right now, and building the brand presence that will matter when they eventually are? Most marketing budgets are allocated almost entirely toward in-market buyers. The 5% showing intent signals. This makes sense given how performance is measured. The organisations that have built durable advantage in their categories consistently show up in the evidence as brands that invested in broad reach and memory-building long before demand emerged.

Where to go next

If you’re dealing with comparable constraints, we’re open to a conversation.